Verification of sustainability reports

Sustainability reports have become increasingly important and are more and more expected or even required as additional accountability from companies. Sustainability reports cover economic, environmental and social issues. Sustainability reports show the progress made each year.

-

- Certification

- Systems and products

- Norms and standards

- Sustainability reports

Verification of sustainability reports

Sustainability reports have become increasingly important and are more and more expected or even required as additional accountability from companies. Sustainability reports cover economic, environmental and social issues. Sustainability reports show the progress made each year.

Summary

In view of the internationally and nationally recognised environmental problems and the existing high explosiveness of this topic in society, a prudent environmental commitment is valuable for all companies today from an ecological, economic and social point of view.

Parallel to the increasing demands in the area of the environment, demands for social responsibility are developing. Fairness in the workplace is expected throughout the entire supply chain.

The constantly growing pressure from relevant interested parties (investors, customers, employees, society, politics, etc.) on sustainability and the constantly changing environmental regulations are creating the demand and, in some cases, the requirement for reporting on activities in connection with sustainability.

If you want to gain the trust of the market, you should prepare a sustainability report that fulfils recognised requirements and have it verified by an independent, objective body.

Development

Sustainability reports emerged as a further development of the environmental reports that emerged in the 1990s.

Sustainability reports cover the following topics: Economy, ecology and social issues (triple bottom line). Alongside the annual report, the sustainability report is becoming an increasingly important part of a company's information policy. It is an instrument of sustainability management and is used by marketing.

There are numerous guidelines and standards for the preparation of sustainability reports:

- GRI

- UN Global Compact

- SDG Compass

- EMAS-procedure

- B-Corp-Standards

These standards overlap to some extent in terms of content, but focus differently on the various aspects of sustainability. In addition to large global companies, medium-sized companies are now also increasingly required to prepare professional sustainability reports. As part of the requirements for supply chains, suppliers are increasingly being asked to provide evidence.

The sustainability reports show the status and progress made in the individual areas:

- Economy: How is the company geared towards the future?

- Ecology: What measures are effectively implemented to protect the environment?

- social issues: How is health promoted, how are social criteria taken into account in procurement?

Orientation aids: Sustainability reports

AccountAbility has developed a solution for companies that want to review their sustainability management, performance and reporting.

The AA1000 Assurance Standard (AA1000AS v3) is a proven methodology used by sustainability professionals worldwide for sustainability-related assurance engagements to assess the nature and extent to which an organisation complies with the AccountAbility Principles.

The AA1000AS v3 is a standard for sustainability testing that:

- A guide:

provides a principle-based guide based on the AA1000 Accountability Principles (2018) of Inclusivity, Materiality, Responsiveness and Impact. - Comprehensive:

Includes a comprehensive, integrated and forward-looking view of an organisation's overall sustainability management, performance and reporting practices. - Applicability:

Ensures flexibility, accessibility and applicability for any organisation, of any size, in any industry, anywhere in the world. - Transparency:

Prioritises user-friendliness to be easy to read, simple to use and clear in its objectives.

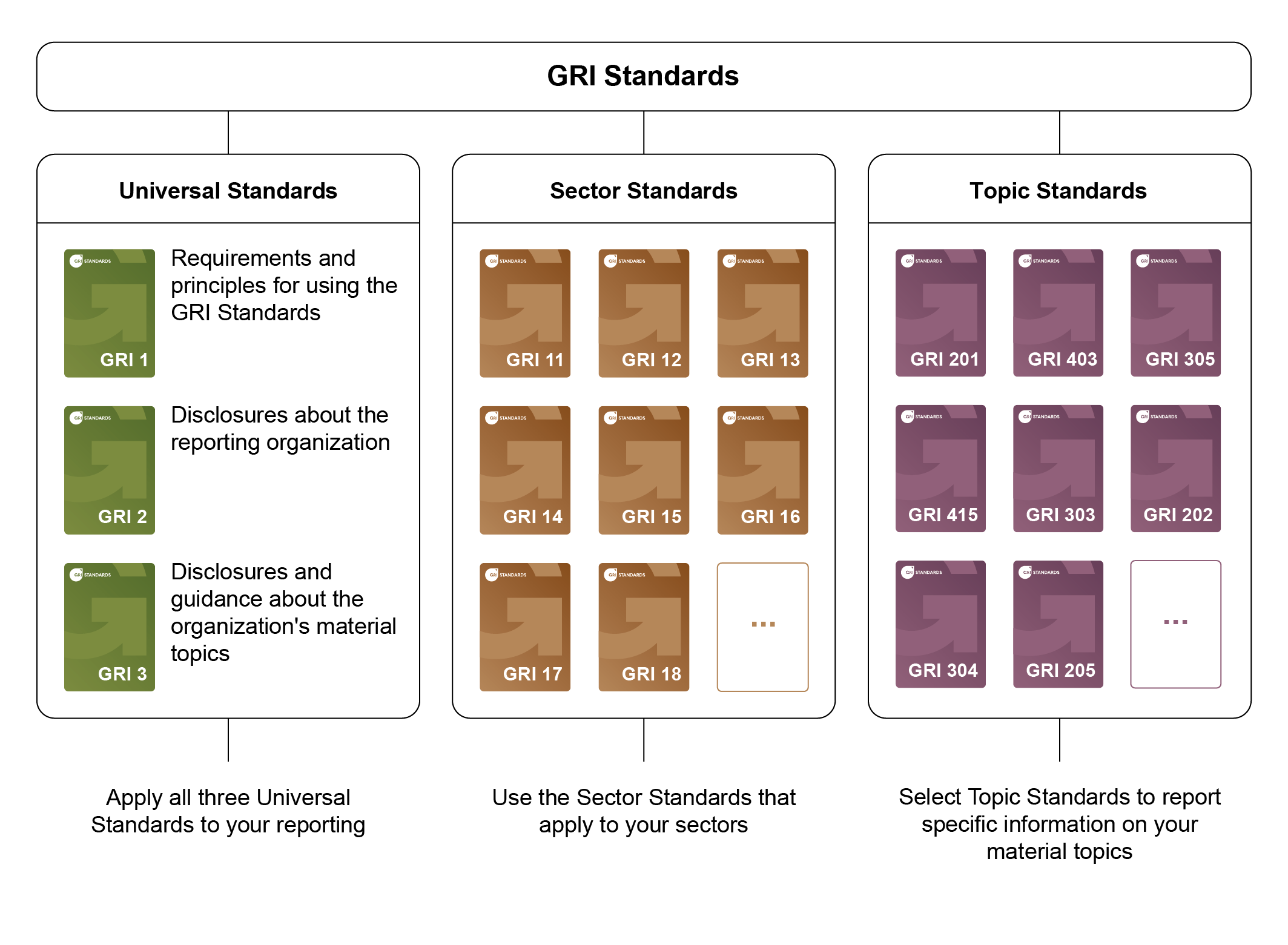

The GRI Standards enable any organisation - large or small, private or public - to understand and report on its impacts on the economy, the environment and people in a comparable and credible way, thereby increasing transparency about its contribution to sustainable development. The standards are not only important for companies, but also for many other stakeholders, including investors, policy makers, capital markets and civil society.

The standards are designed as an easy-to-use, modular set that provides a comprehensive picture of an organisation's material issues, the associated impacts and the way they are managed.

{kind=link}

- The Universal Standards - recently revised to include reporting on human rights and environmental due diligence in line with intergovernmental expectations - apply to all organisations;

- The new sector standards enable more standardised reporting on industry-specific impacts;

- The thematic standards - adapted to the revised Universal Standards - list the information relevant to a specific topic.

As part of the implementation of the CSRD, the EU Commission has commissioned the European organisation EFRAG to define mandatory European reporting standards.

In future, all companies in the EU that are subject to the requirements of the Corporate Sustainability Reporting Directive (CSRD) will have to apply the European Sustainability Reporting Standards (ESRS) in their reporting.

The Sustainable Development Goals (SDGs) are to be achieved globally and by all UN member states by 2030. This means that all countries are equally called upon to work together to solve the world's pressing challenges. Switzerland is also called upon to implement the goals nationally. Incentives should also be created to encourage non-state actors to make a more active contribution to sustainable development.

17 Sustainable Development Goals:

- End poverty in all its forms and everywhere

- End hunger, achieve food security and better nutrition and promote sustainable agriculture

- Ensure a healthy life for all people of all ages and promote their well-being

- Ensure inclusive, equitable and quality education and promote lifelong learning opportunities for all

- Achieve gender equality and empower all women and girls

- Ensure availability and sustainable management of water and sanitation for all

- Ensure access to affordable, reliable, sustainable and modern energy for all

- Promote lasting, broad-based and sustainable economic growth, full and productive employment and decent work for all

- Build resilient infrastructure, promote inclusive and sustainable industrialisation and foster innovation

- Reducing inequality within and between countries

- Making cities and neighbourhoods inclusive, safe, resilient and sustainable

- Ensuring sustainable consumption and production patterns

- Take immediate action to combat climate change and its effects

- Conserve and sustainably utilise oceans, seas and marine resources for sustainable development

- Protecting and restoring terrestrial ecosystems and promoting their sustainable use

- Promoting peaceful and inclusive societies for sustainable development

- Strengthening the means of implementation and revitalising the Global Partnership for Sustainable Development

With the rejection of the Responsible Business Initiative on 29 November 2020, Parliament's indirect counter-proposal was approved. The provisions of the counter-proposal entered into force on 1 January 2022.

The counter-proposal consists of two parts:

- Provisions on transparency regarding non-financial matters (Art. 964a to Art. 964c CO)

- Provisions concerning due diligence obligations and transparency with regard to minerals and metals from conflict areas (conflict minerals) and child labour (Art. 964j to Art. 964l CO). The second part is covered by the Ordinance VSoTr.

The provisions are mandatory for public companies within the meaning of Art. 727 of the Swiss Code of Obligations and FINMA-supervised organisations, provided that they have been in existence for two consecutive financial years:

at least 500 full-time positions on an annual average and

at least one of the following figures has been exceeded: Balance sheet total of CHF 20 million or sales revenue of CHF 40 million

Companies that are controlled by another company that is required to prepare a report in accordance with Art. 964a of the Swiss Code of Obligations or an equivalent report under foreign law are exempt from reporting.

Elements of transparency and accountability:

- Environmental issues

- Social issues

- Labour issues

- Respect for human rights

- Combating corruption

Required information:

- Describe the business model (how is added value achieved?).

- Concepts with which the objectives of the concerns are pursued.

- Presentation of the measures taken to implement the concepts and the evaluation of the effectiveness of the measures.

- Description of risks and risk management.

- Disclosure of performance indicators in relation to the 5 issues.

As things stand at present, no independent review of the report is planned.

(Based on the procedure in the EU, this could still change).

Switzerland: 2030 Agenda for Sustainable Development.

With ISO 26000, ISO has created a framework that supports companies in improving their corporate social responsibility (CSR) and establishing a socially responsible organisation. It summarises the principles of action and core topics of corporate social responsibility. Unfortunately, the standard was not formulated as a management system standard with certifiable requirements. As a guideline for social responsibility, it helps to promote responsible behaviour within the company in the sense of a continuous improvement process.

It is a comprehensive guide (149 pages) covering the following topics:

- Terminology

- Understanding social responsibility

- Principles of social responsibility:

Accountability, transparency, ethical behaviour, respect for stakeholder interests, the rule of law, international standards of conduct, human rights - Recognising social responsibility and involving stakeholders

- Recommendations for action on the core issues of social responsibility:

Human rights, labour practices, environment, fair operating and business practices, consumer concerns,

community involvement and development - Recommendations for action for the organisation-wide integration of social responsibility

- Comparison of examples of voluntary initiatives and tools (Appendix A)

Creation of sustainability reports

Creating a sustainability report is a structured process that requires careful planning and commitment. Here are the basic steps that companies typically follow to create a comprehensive sustainability report:

1. Preparation and planning

- Objective: Define what the report should achieve, e.g. increase transparency, inform stakeholders, fulfil legal requirements.

- Identifying stakeholders: Determine who the report's target groups are (investors, customers, employees, etc.).

- Materiality analysis: Determine which topics are most relevant for your stakeholders and your business. This helps to focus the content of the report.

2. Data collection

- Determine data sources: Identify internal and external data sources.

- Data collection: Collect quantitative and qualitative data on the previously defined material topics. This can include environmental performance, social initiatives, governance practices and more.

3. Selecting reporting framework and standards

- Standard selection: Decide which reporting standards (e.g. GRI, AA1000, ISO 26000) and which legal regulations must be observed.

- Developing a structure: Create an outline based on the chosen standards and the most important topics.

4. Reporting

- Write content: Formulate clear and precise information on each key category. Include successes as well as challenges and failures.

- Visualising data: Use diagrams, tables and infographics to present complex data in an understandable way.

- Case studies and examples: Include specific examples and case studies that illustrate your data and statements.

5. Inspection and validation

- Internal examination: Have the report reviewed by different departments (e.g. legal, finance, marketing).

- External examination: Engage external experts or auditors to verify the accuracy and credibility of the information.

6. Publication and communication

- Publication: Publish the report in a format that is accessible to your target groups (e.g. PDF, interactive online platform).

- Communication: Develop a communication strategy to effectively disseminate the report, including press releases, social media, webinars and presentations.

7. Feedback and improvement

- Obtain feedback: Gather feedback from stakeholders on the quality and usefulness of the report.

- Optimisation process: Use the feedback to continuously improve the reporting process and adapt future sustainability strategies.

This process requires a clear vision, good management of available resources and a willingness to report transparently and honestly on the company's sustainability performance.

Do not underestimate the effort required to obtain the data.

The most efficient and effective approach is to determine the report structure and content and then collect the data over a period (one year). At the end of the period, the data is processed and analysed to create the report.

Verification of sustainability reports

To increase credibility and trust, the sustainability report can be verified by an independent institution such as the Swiss Safety Centre.

As part of the audit, the accuracy of the data and its correct determination and recording is assessed.

We will be happy to discuss the procedure with you.

Utilisation & Benefits

Sustainability reports have several important functions that are beneficial for companies themselves as well as for their stakeholders and society in general. Here are some of the most important benefits they provide:

- Transparency: Sustainability reports increase the transparency of corporate activities in the area of social, economic and environmental sustainability. They enable stakeholders to better understand the impact of the company's activities on the environment and society.

- Accountability: Through reporting, companies can demonstrate their responsibility to stakeholders such as investors, customers, employees and society. These reports show how seriously a company takes its sustainability commitments and promote trust.

- Risk management: Sustainability reports help companies to identify and manage risks that may arise from environmental, social and governance (ESG) factors. This can also include financial risks that may arise from climate change, resource scarcity or social unrest.

- Improving corporate governance: By regularly collecting and analysing data for the sustainability report, companies can identify areas where they can improve their practices. This promotes better decision-making and more efficient processes.

- Brand value and competitive advantage: A comprehensive and convincing sustainability report can improve the brand image and create a competitive advantage. Companies that are perceived as sustainable can attract customers and investors who value environmentally friendly and socially responsible business practices.

- Compliance with legal regulations: In many countries, companies are required by law to report on certain aspects of sustainability. These reports help to fulfil compliance requirements and avoid penalties or legal disputes.

- Stakeholder-Engagement: Sustainability reports provide a platform for dialogue and engagement with various stakeholders. They enable stakeholders to provide feedback and actively participate in shaping the company's sustainability strategy.

- Attractiveness for investors: Sustainability reports are often a decisive factor for investors looking for sustainable investments. They provide the detailed information investors need to assess the long-term potential and sustainability of business models.

Through these diverse functions, sustainability reports help companies not only to achieve their own operational goals, but also to make a positive contribution to society and the environment.

What you need to know

The requirements for sustainability reports result from the needs of stakeholders and legal requirements:

EU: see ESRS

Switzerland: see Transparency on non-financial matters, 964 OR

As an aid for your company, you can download the audit checklists from the ‘safetycenter-shop’ free of charge.

You will find checklists for the area of sustainability:

- ISO 14001

- ISO 26000

Sustainability reports are an essential part of a company's communication about its environmental, social and governance performance. Here are some important things to know about sustainability reporting:

Standards and frameworks:

There are various standards and frameworks for the preparation of sustainability reports. These guidelines help companies to structure their reports and ensure that they provide relevant and comparable information.

Materiality:

The term ‘materiality’ is central to sustainability reporting. Companies should focus on topics that are of the greatest importance to their business activities and their stakeholders. This means that not all environmental or social issues are equally relevant for every company.

Data quality and integrity:

The quality and integrity of the data used in sustainability reports is crucial. Companies must ensure that the data is reliable, accurate and verifiable. External audits by third parties can help to increase the credibility of the reports.

Communication and transparency:

An effective sustainability report should not only be informative, but also clear and understandable. It should provide an honest assessment of the company's sustainability performance and challenges and also highlight areas for future improvement.

Regular updates:

Sustainability reports should be published regularly to reflect the current status of a company's sustainability efforts. Most companies publish annual reports to enable an ongoing assessment of their progress and challenges.

Stakeholder-Engagement:

Stakeholder engagement is an important part of the process. Companies should consider feedback and expectations from customers, employees, investors and other relevant groups in order to improve their sustainability strategies and reports.

Reporting on negative effects:

Honesty in reporting on failures or negative impacts is crucial. Companies should report transparently on areas where they have not met their targets or have had a negative impact. This shows a commitment to real improvement and responsibility.

Orientation towards the future:

In addition to reporting on past and present performance, sustainability reports should also include future goals and plans for sustainable development. This helps stakeholders to understand how the company intends to achieve its long-term sustainability goals.

Sustainability reports are not just documentation of performance or a PR measure, but an important tool for strategic control, risk management and strengthening the brand in the context of sustainability.

Courses of the Swiss Safety Centre Academy

We offer seminars on the topic of sustainability reporting: